Why digital instruments on traditional rails leave the capital problem intact

Author: Maximilian Hartmann | Senior Marketing & PR Manager @21X

This article examines why the structural separation of trade matching from settlement creates systemic capital inefficiency in traditional capital markets. It addresses why digitizing existing processes is not sufficient and identifies atomic, on-chain settlement as the mechanism that resolves this constraint. Tokenization of assets alone cannot eliminate counterparty risk without a fundamental change to the settlement infrastructure beneath it.

Every securities trade in traditional capital markets contains a structural delay. The moment a buyer and seller agree on a price, the transaction does not settle – it enters a clearing process that spans two business days. During those two days, neither party has concluded the exchange. The seller has not yet been paid, the buyer does not yet legally hold the asset. Capital is locked, operationally committed but financially idle.

This T+2 cycle is not incidental – it reflects decades of infrastructure built around private, disconnected ledgers – each custodian, central counterparty (CCP), and central securities depository (CSD) maintaining its own record of ownership. Reconciling these records across institutions requires time, and that time has a cost. Institutions post margin at central counterparties and hold regulatory capital against settlement exposures. Institutions post margin against counterparty risk that would not exist if settlement were immediate.

As tokenized financial instruments move from pilot projects to active secondary markets, this settlement gap has become impossible to ignore. Digitizing the front end of capital markets without replacing the underlying settlement rails does not solve the structural problem. It only makes it more visible.

The cost of the gap between trade and ownership

The settlement cycle does not merely delay the transfer of assets – it creates an interval of structural risk that the entire financial system is organized around managing. During T+2, both buyer and seller are exposed to the possibility that the other party fails to deliver. This is why CCPs exist: they step between buyer and seller, becoming the legal counterparty to each side through a process called novation, and absorbing the credit risk of the interval.

This risk management architecture is effective, but it is expensive. Margin requirements, default funds, and collateral obligations lock up capital that cannot be deployed elsewhere. For market participants operating across hundreds of positions simultaneously, the aggregate drag is material. Aggregated across positions, a material portion of balance-sheet capacity is consumed not by investment activity, but by the friction of waiting for trades to settle.

Efforts to compress settlement cycles – from T+2 to T+1, as implemented in US equity markets in 2024 and adopted in the EU and UK from October 2027 – reduce the exposure window but do not eliminate the structural problem. As long as matching and settlement are separate events handled by different entities on different ledgers, some version of this gap, and the capital cost it generates, will persist.

Atomic settlement as a structural mechanism

Distributed ledger technology (DLT) addresses the settlement gap not by compressing the cycle further, but by eliminating it entirely. In an on-chain settlement model, trade matching and final ownership transfer occur within a single blockchain transaction. The mechanism is called ‘atomic settlement’: the asset token moves to the buyer’s wallet and the payment moves to the seller’s wallet simultaneously, or neither transfer occurs. There is no interval between these events.

This is a structural change, not an incremental improvement. Tokenized instruments that still settle through traditional rails keep the gap intact only the front end is digital. Because both legs of the trade settle in the same transaction, counterparty risk is removed by the logic of the protocol rather than managed by an intermediary. A CCP is no longer necessary to absorb the credit risk of the settlement interval, because the interval no longer exists. Capital previously committed as margin or collateral against this risk becomes available immediately upon trade execution.

For this mechanism to function in regulated capital markets, the smart contract executing the settlement must operate within a compliant framework. Participants must be verified, assets must be issued under a legal structure, and the settlement system must meet regulatory standards. This is precisely the combination that the EU’s distributed ledger technology (DLT) Regime was designed to enable – and that 21X is the first exchange to have implemented under a full license.

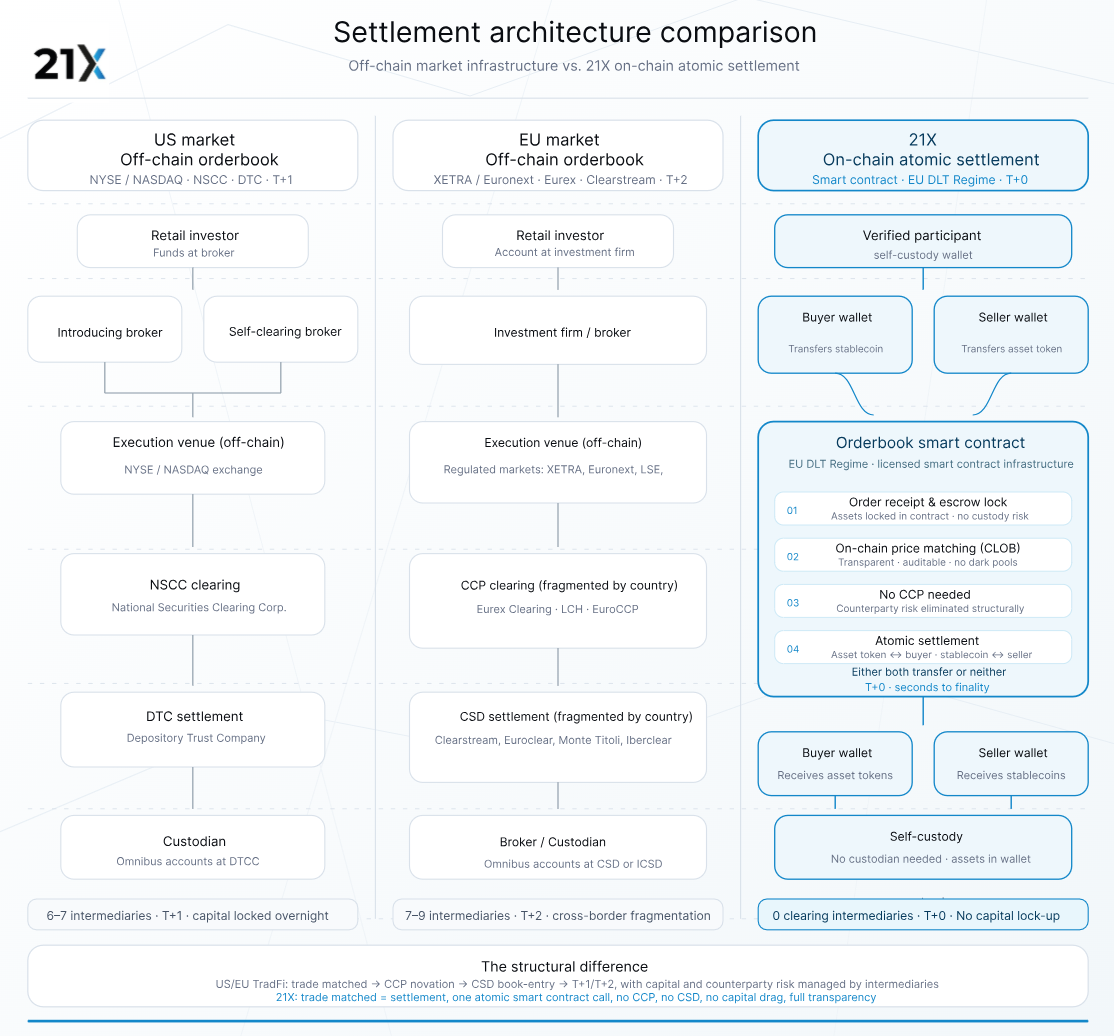

How atomic settlement operates in practice on 21X

The operational sequence on 21X makes the structural difference concrete. Before a trade can occur, onboarded buyers hold stablecoins in their own wallets; onboarded sellers hold tokenized asset instruments in theirs. When a buyer places a limit order, the stablecoins transfer directly into the on-chain orderbook smart contract. When a seller places a corresponding order, the asset tokens follow. The assets of both parties are held by the protocol, not by an intermediary.

When the limit prices match, the smart contract executes the settlement in the same transaction: asset tokens move to the buyer’s wallet, stablecoins move to the seller’s wallet. The entire lifecycle – from order placement to final ownership transfer – is completed within a single blockchain transaction. There is no post-trade process, no reconciliation, and no settlement window.

“Secondary market liquidity is essential to ensure that tokenized instruments function as usable treasury assets rather than long-term locked positions.”

This points to a broader principle: settlement efficiency and secondary market liquidity are not separate concerns – they are interdependent. A trade that settles atomically creates an immediately available position, enabling faster reinvestment and tighter collateral management.

“True efficiency gains in tokenized markets only emerge when issuance, trading, and settlement are combined on a single regulated DLT-based market infrastructure.”

Fig 1. Settlement architecture comparison, source. 21X 2026

Settlement as the defining variable

The structural problem of capital markets is not the absence of digital instruments – it is the persistence of a settlement architecture that separates the moment of agreement from the moment of finality. As long as that gap exists, capital is committed to managing it rather than generating returns.

Atomic settlement, implemented through smart contracts on a regulated distributed ledger, closes this gap by design. The mechanism does not compress the settlement cycle – it eliminates the distinction between trade execution and settlement entirely. For institutions evaluating tokenized markets, the relevant question is no longer whether DLT can handle institutional volume. It is whether the settlement infrastructure beneath a given platform is capable of removing the capital drag that T+2 and its variants have made structurally endemic.

21X is now live as the first fully licensed DLT trading and settlement system in the EU, providing a regulated environment in which this mechanism operates at scale.

If your institution is assessing how atomic settlement can reduce capital drag and settlement risk within your existing regulatory framework, the 21X team is available to walk through the operational and compliance structure in detail.