Money market funds show you how.

As tokenized funds move from pilots to institutional workflows, the buy-side question is shifting from access to utility.

Author: Maximilian Hartmann

Money market funds are emerging as one of the clearest buy-side use cases for tokenized markets as institutions look for ways to combine yield, transferability and collateral mobility within a regulated digital market infrastructure.

The relevance is not that every investor can suddenly access every fund. It is that regulated fund interests can become easier to transfer, trade, settle and use when they are inside market infrastructure tailored for digital assets.

Why money market funds are the practical test

Money market funds are not usually treated as innovation stories. They are operational instruments. Asset managers, treasury desks, market makers, brokers, digital asset firms and institutional investors use them to manage short-term liquidity, preserve capital and generate yield on cash-like positions.

That is precisely why they matter. Despite the interest created by real world assets (RWAs) such as fractionalized real estate, the first credible wave of large-scale tokenization was not defined by exotic assets. Instead, it started with instruments that are already understood, already regulated and already central to institutional workflows. Government bonds and money market funds fit that pattern.

A traditional money market fund solves the yield problem. A stablecoin solves the mobility problem. A tokenized money market fund attempts to connect both: Yield-bearing exposure, with digital transferability.

Comparing liquidity products – from access to utility

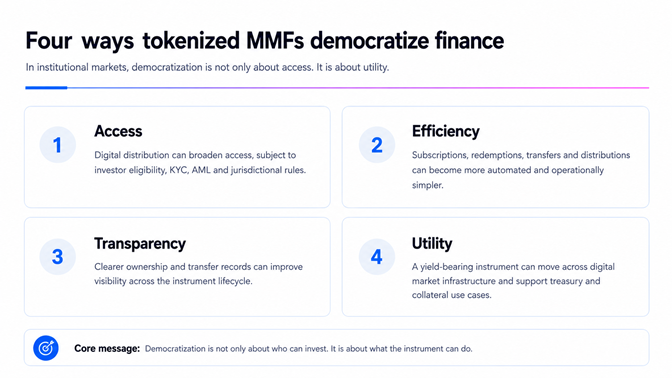

The common definition of democratization in finance focuses on access. That certainly matters, but it is too narrow a definition. For the buy side, utility is often more important than access alone as it offers:

- Better access through digital distribution, subject to investor eligibility, know-your-customer (KYC), anti-money laundering (AML) and jurisdictional requirements.

- Greater operational efficiency through more automated subscriptions, redemptions, transfers and distributions.

- Improved transparency through clearer ownership and transfer records.

- Greater utility by allowing a yield-bearing instrument to move across digital market infrastructure.

The new asset is mobile yield

For institutional investors liquidity cannot sit still. It has to move, settle, meet margin requirements, and be posted as collateral. Most importantly, it has to be redeployed the moment markets shift.

In a tradfi world, a fund interest may be economically liquid but operationally slow. Cut-off times, transfer agent processes, fund platform dependencies, bank settlement windows and custody silos limit how quickly the position can be used.

But in a defi world, the fund interest can become wallet-native. That does not, however, mean it becomes unregulated or freely transferable to anyone. It means the transfer logic, eligibility rules and settlement process can be embedded into the infrastructure.

A tokenized money market fund is not just a fund share in digital form. It can become a yield-bearing collateral asset that is easier to move, settle and integrate into institutional workflows.

Why this matters for the buy side

The buy side does not need tokenization for its own sake. It needs better market function. The practical question is not whether a fund share can be represented on a blockchain, . but whether that representation improves liquidity management, collateral mobility, settlement certainty, treasury efficiency and operational control. Tokenized money market funds offer a compelling solution because they address a real trade-off.While cash is liquid but often produces limited yield, stablecoins are digitally mobile but are not money market funds and do not provide the same regulated fund exposure. Traditional money market funds can provide yield, but they are not built natively for continuous digital transfer and settlement.

The market structure constraint

A token alone does not create a market. It does not automatically create liquidity, price discovery, custody, regulatory certainty or collateral utility.

That is the main limitation behind many tokenization narratives. Representing an asset on a distributed ledger does not guarantee secondary market depth. It does not remove compliance requirements. It does not solve the legal relationship between the token, the asset and the investor. It does not replace the need for regulated infrastructure.

Tokenized securities remain securities. Tokenized fund interests still require compliance. Investor eligibility still matters. Custody still matters. Market abuse rules still matter. Disclosure still matters. Settlement finality still matters. This is not a weakness. It is the condition for institutional adoption.

The infrastructure layer is decisive

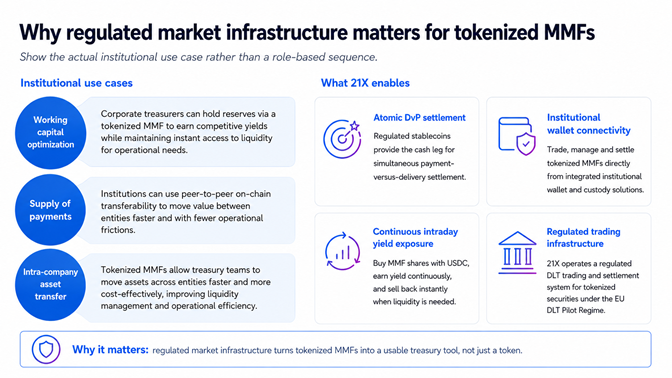

The market function emerges only when issuance, trading and settlement are connected in a regulated environment.

The more important questions begin after issuance: Can the instrument be traded? Can settlement occur atomically? Can payment and asset transfer happen simultaneously? Can eligible participants interact under clear rules? Can the instrument become part of broader collateral and liquidity workflows?

21X is regulated market infrastructure for tokenized securities. It enables issuers and institutional participants to connect issuance, trading and settlement in a distributed ledger technology trading and settlement system (DLT-TSS), authorized under the European Union DLT Pilot Regime and licensed by BaFin.

Atomic settlement is central to this model. Asset transfer and payment transfer occur simultaneously. The settlement window is reduced. Counterparty exposure is reduced. Capital is not left idle during the time between trade execution and settlement.