What Tokenization Is and What It’s Not

by Andy Do Tuan, Senior Business Development Manager @21X

and Benjamin Schellinger Business Operations Manager @21X

In Part 1, tokenization was defined as an evolution in infrastructure technology; a pragmatic continuation of existing market structures in which assets are transformed into native digital, programmable market objects. This definition creates legal continuity and regulatory clarity, enabling market participants to view tokenization as a credible infrastructure option rather than a speculative concept. To underscore the shift from speculation to utility, note that tokenization is increasingly viewed as a bridge between traditional finance and digital networks, with institutions like Citi highlighting its potential to “re-architect capital markets” through programmability and composability.

In Part 2, the focus shifts from conceptual differentiation to practical implementation. The article examines how distributed ledger technology and smart contracts are already being used in practice today, where institutional adaptation is visible, and what framework conditions will shape the next scaling phase. Particular attention is paid to how regulated platforms such as 21X are operationally implementing the concept of an end-to-end, compliance-by-design tokenization infrastructure and what strategic implications this has for professional market participants.¹ ⁴ ⁵

Why DLT and smart contracts are crucial

Distributed ledger technology should not be understood as a “better database.” Its relevance lies in a fundamentally different infrastructure logic with direct implications for trading, settlement, and post-trade processes.¹

- Single source of truth: Ownership and entitlement rights are recorded in a legally relevant register, eliminating the need for time-consuming coordination between central securities depositories and custody systems while reducing operational complexity.¹

- Programmable rights and processes: Interest payments, redemptions, corporate actions, and voting rights are executed on a rule-based basis via smart contracts, reducing manual intervention and operational risks.¹ ²

- Atomic settlement: Delivery and payment take place simultaneously in a single transaction, rather than via sequential message chains. Settlement cycles are shortened and counterparty risks are reduced. Additionally, note privacy enhancements in hybrid models, where zero-knowledge proofs can maintain compliance without exposing sensitive data on public chains

Market status: Between pilot wave and institutional adaptation

In Germany and Europe, concrete progress in tokenization is increasingly evident. Banks have obtained licenses for crypto custody and crypto securities registers, and the first tokenized bonds, money market instruments, and fund shares have been issued under regulatory supervision. Pilot transactions with established market participants show that end-to-end processes—from issuance to settlement—are already working in practice.

These activities are currently focused on market segments where regulatory clarity, market structure, and operational maturity converge:

- Tokenized securities are the focus of early implementation because they have liquid reference markets, clear legal frameworks, and established issuance and post-trade processes.

- Tangible assets such as real estate, art, or collectibles remain in an experimental phase, limited by low liquidity, fragmented market structures, and a lack of standardization.

- Standardized fixed-income segments are showing the strongest momentum. Studies by Roland Berger and Citi identify private credit, government bonds, money market products, and fund structures in particular as key drivers of short-term development.¹ ⁴

Despite this progress, tokenized instruments still account for only a small share of the overall capital market. The industry is still in a phase of infrastructural preparation and has not yet undergone a comprehensive transformation. Standardization, liquidity creation, and integration into existing market and distribution networks are crucial for scaling.¹ ²

Key challenges and prerequisites for scaling

The reasons why institutional breakthroughs have not yet occurred can be divided into two categories:

- Investment and transformation costs: Setting up DLT-based infrastructures require significant initial investments, often in the double-digit million range. Established institutions must operate existing and new settlement infrastructures in parallel. Whether efficiency gains of around 25% in issuance and up to 50% in post-trade more than offset the migration costs depends on size and strategic orientation. ²

- Fragmentation of the DLT landscape: Market participants use different architecture models, which leads to interoperability problems. Instead of simplification, initially this creates additional complexity.¹ ⁴

- Private blockchains: Used by banks and consortia for complete control over governance and compliance. Suitable for regulated pilot projects, but lead to isolated systems with limited interoperability.

- Public blockchains: Open networks with high scalability. Increasingly used for tokenized funds and money market products, but pose challenges in term of regulatory integration and data protection.

- Hybrid models: Combine public ledger infrastructure with permissioned access and compliance layers. Attempt to combine openness and control, but increase technical complexity.

Structural inertia of established capital markets

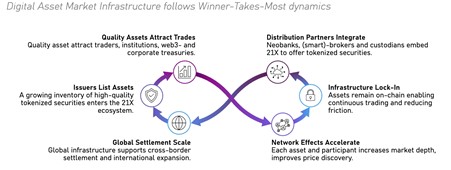

Established capital markets are characterized by strong network effects: Existing infrastructures are highly standardized, reliable, and deeply liquid. These characteristics reinforce each other’s liquidity, attract participants which then attract issuers, and issuers deepen liquidity.

Tokenized instruments initially operate outside these feedback loops. Even with technical and regulatory maturity, limited distribution, fragmented liquidity and a lack of trading networks limit the incentives for rapid migration.

Prerequisites for scaling

- Compliance-enabled use of open DLT systems: Open networks enable interoperability but require regulatory requirements such as investor qualification and transfer restrictions to be mapped directly into smart contracts.

- Common standards: Uniform data models, asset taxonomies, and smart contract frameworks are prerequisites for interoperability and scaling. Initiatives such as Project Guardian demonstrate how standardization reduces fragmentation.

Practical relevance: 21X as a regulated DLT market infrastructure

The central question for institutional market participants is no longer whether tokenisation is technically feasible, but which market infrastructures are capable of implementing it in a way that is both regulatorily compliant and operationally viable at scale.

21X addresses this question as the first operator of a fully regulated DLT Trading and Settlement System (DLT TSS) under Regulation (EU) 2022/858.⁵ Structurally, the platform combines two functions that have traditionally been separated:

- a DLT Multilateral Trading Facility (DLT MTF) enabling smart-contract-based trading and direct market participation, and

- a DLT Settlement System (DLT SS) providing on-chain securities registration and settlement, including delivery-versus-payment logic.

By integrating trading, settlement, and registry functions within a single DLT-based infrastructure, 21X establishes a single source of truth for tokenised instruments. Settlement can occur in an atomic, T+0-like manner, while compliance requirements such as transfer restrictions, eligibility rules, and lifecycle events are embedded directly into smart contracts.

Crucially, 21X does not position tokenisation as a standalone product layer, but as an infrastructural capability that supports both primary issuance and secondary market trading on the same regulated platform. The initial focus on core institutional instruments – including money market products, short-term securities, and fund units – reflects where standardisation, liquidity potential, and regulatory clarity already converge.

In this sense, 21X serves as practical evidence that tokenised market infrastructure can already operate today within the European regulatory framework, not as a pilot environment, but as an exchange-like venue designed for institutional use.

Conclusion and implications for market participants

This article has shown that the critical challenge for tokenisation is no longer conceptual clarity, but infrastructure execution.The central challenge of tokenization no longer lies in conceptual classification, but in infrastructural implementation. Scaling requires platforms that combine regulatory depth, integrated trading and settlement, and the ability to trigger network effects.

For professional market participants, these insights translate into clear strategic imperatives:

- Tokenization should be addressed through regulated market infrastructures, not isolated technical experiments.

- Early participation through pilot issuances or trading standardized instruments creates operational experience and strategic options.

- When selecting partners, regulatory connectivity, interoperability, and exchange-like maturity should be the focus not narrative promises.

Tokenization holds significant potential to transform capital market infrastructure. Platforms such as 21X, operating under the EU DLT Pilot Regime, demonstrate that regulated, fully functional DLT trading and settlement systems are already a reality. These infrastructures enable faster settlement, programmable compliance, and integrated trading and settlement on a single platform. As standardisation advances and network effects materialise, tokenization is poised to become a core component of modern capital markets. Early engagement with pioneers like 21X will enable market participants to shape this transformation and capture the efficiency gains it offers.

References

¹ Citi GPS (2023). Money, Tokens and Games.

² Deloitte (2019). The tokenisation of assets is disrupting the financial industry.

³ Cremers, M. (2024). Tokenisation and the Banking System.

⁴ Roland Berger (2023). RWA Tokenisation Market Outlook 2030.

⁵ European Commission (2022). Regulation (EU) 2022/858 — DLT Pilot Regime.

⁶ Liechtenstein: Token and VT Service Provider Act (TVTG), LGBl. 2019 No. 301. ⁷ Switzerland: Federal Act on the Adaptation of Federal Law to Developments in Distributed Ledger Technology (DLT Act), in force since 2021; in particular amendments to the Book-Entry Securities Act (BEG).