Author: Nicolas Klose, Business Analyst at 21X

Stablecoins, deposit tokens and central bank digital currencies are racing to fill the cash leg of on-chain markets. Interoperability with wallet infrastructure and smart contracts will determine whether asset tokenization delivers atomic settlement or remains a partial fix.

Capital markets are adopting tokenized assets as a new form of value transfer with blockchain technology to keep a transparent, tamper-proof shareholders registry. While tokenized securities tend to follow a dominant design pattern being issued on leading public blockchain infrastructures, the standardization of tokenized cash is more difficult.

Securities can now be issued, traded and transferred natively on distributed ledger infrastructures. From a technological perspective, the asset leg of capital markets has advanced faster than the market structures built around it. The bottleneck sits elsewhere – in the cash leg. As long as payments remain off-chain, tokenized markets remain structurally incomplete and unable to take advantage of the benefits that the blockchain promises.¹ Tokenized forms of cash needs to act as a stable store of value, while reaching physical money in the level of security, trust, accessibility and transferability. Additionally, digital money needs to be programmable, by ensuring smart contract interoperability and compatibility with wallet infrastructure. This is why stablecoins – in the form of regulated e-money tokens, tokenized bank deposits and, eventually, central bank digital currencies are no longer peripheral innovations. They are the foundation of modern capital market infrastructure, enabling atomic delivery-versus-payment with finality and zero counterparty risk. Without them, tokenization remains just an incremental improvement.²

Fig 1: Source 21X

When money becomes programmable, settlement changes

Digital money has expanded steadily over the past decade, driven by e-commerce, globalization and automation. The structural shift begins where digital money intersects with distributed ledgers and smart contracts. At this point, money becomes programmable.

The German Federal Bank defines programmable money as a digital form of money that follows an inherent logic for a predefined purpose, based on the properties of the money itself.³ In this model, money is no longer merely transferred; it becomes embedded in an executable process.

As early as 2020, the Bundesbank outlined use cases ranging from cross-border payments and machine-to-machine transactions to trade finance and peer-to-peer transfers.³ In capital markets, the implication is direct: money becomes part of trading, matching and settlement logic. Infrastructure that supports programmable money allows market participants to align settlement flows with execution logic rather than reconcile them afterwards. Instead of settling through banks and financial intermediaries connected to real-time gross settlement systems (RTGS) such as TARGET2 and Fedwire over several days, programmable – in this case tokenized – money can settle instantly in a peer-to-peer fashion.

Collapsing the separation between asset and cash

Traditional capital markets are built on robust but fragmented architecture. Securities move through central securities depositories, while payments move through separate banking systems. Time lags, intermediaries and collateral frameworks historically bridged the gap.

DLT-based models collapse this separation. The breakthrough occurs when both sides of a transaction are digitized and synchronized. Rather than relying on hybrid settlement models or off-chain workarounds, asset and cash operate on a shared infrastructure layer. The asset and the cash settlement of a securities trade do not longer need to be two separate processes – in tokenized form, they settle instantly within one single blockchain transaction.

True delivery-versus-payment emerges from this synchronization. Settlement becomes atomic, reducing credit exposure and operational latency. In this context, digital money is not simply a payments innovation. It is settlement infrastructure.

A spectrum of digital money

Digital money differs less by technology than by regulatory classification and institutional design. Within the European Union, MiCAR provide the framework that differentiates between three different types of crypto assets.⁴⁵

Cryptocurrencies such as Bitcoin or Ether and especially stablecoins demonstrate how value can move on-chain efficiently. However, absent issuer liability and supervisory alignment, they do not meet the requirements of settlement money in regulated markets.

Asset-Referenced Tokens reference baskets of assets. While structurally stable, their multi-asset composition introduces added complexity from a legal and risk perspective, making them less straightforward as a wholesale settlement leg.

E-Money Tokens represent a regulated subclass of stablecoins, combining the efficiency and utility of on-chain value transfer with legal certainty and oversight of traditional financial instruments. They reference a single official fiat currency and are issued by licensed institutions under MiCAR and the E-Money Directive.⁴⁶ They are fully backed, redeemable at par and legally enforceable. In regulated environments, they currently represent the most operationally compatible digital cash solution by ensuring wallet accessibility, programmability, transferability, and institutional trust.

Fig 2: Source 21X

For capital markets, the decisive factor besides the technical token design is whether the instrument operates within a framework that ensures legal certainty, clear liability and supervisory alignment.

“Tokenized markets require digital cash that can settle with finality on public networks within a European regulatory perimeter,” says Nicolas Klose, Business Analyst at 21X. “E-money tokens enable atomic settlement when integrated into DLT-based trading infrastructure such as 21X’s trading platform.”

E-Money Tokens as a pragmatic reality

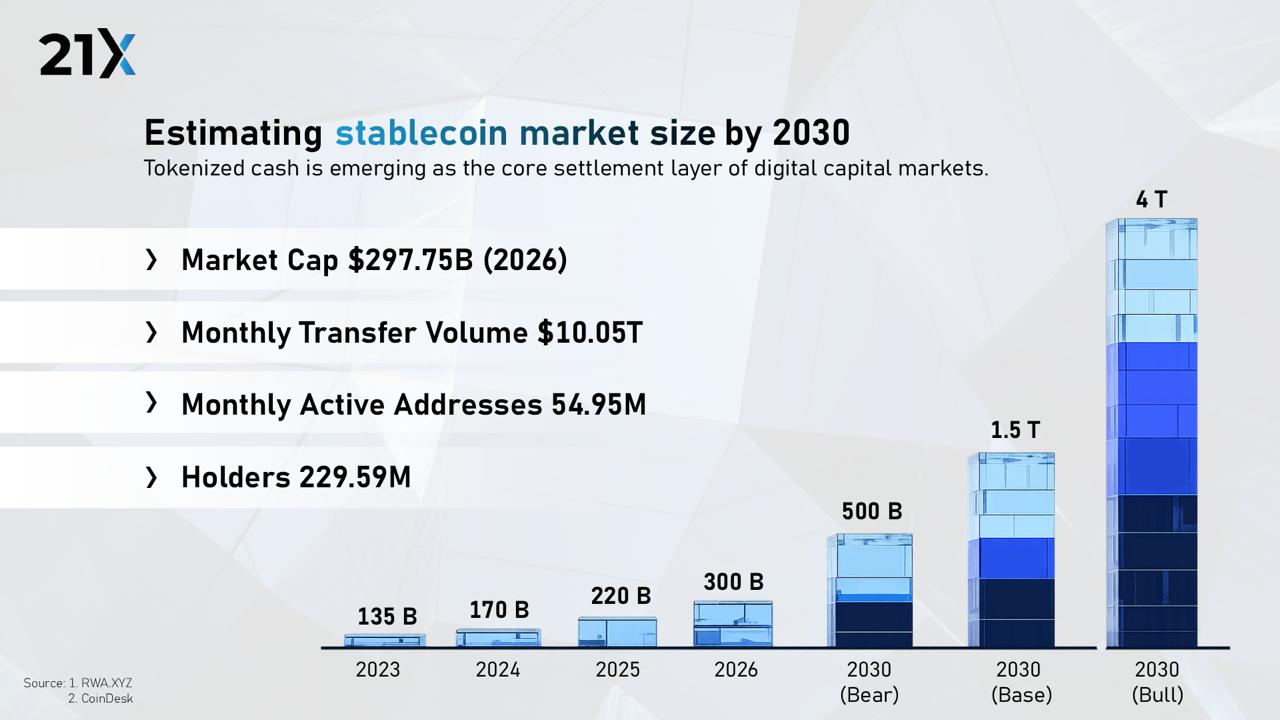

At this moment, already more than ten issuers received an E-money token license in Europe⁴⁶, and their e-money tokens already facilitate daily transfer volumes in the millions of euros.

Within this framework, AllUnity’s stablecoins (EURAU and CHFAU) represent euro- and Swiss franc–denominated, MiCAR-compliant e-money tokens designed for regulated financial market use cases, including payments, settlement and treasury flows.

“AllUnity’s stablecoins are built for institutional integration,” adds Rupertus Rothenhäuser, CCO at AllUnity. “Fully compliant and fully backed, they provide secure, regulated digital cash for institutional use. They enable businesses to settle payments instantly, around the clock, with lower costs and greater capital efficiency.”

E-money tokens therefore allow the industry to execute delivery-versus-payment today, without waiting for the longer development cycle of wholesale central bank digital currency infrastructure.

Conclusion

Tokenized markets have solved the asset leg. The scaling question now sits with the use of programmable and trustworthy digital forms of money.

As long as the cash leg remains structurally separate, tokenization delivers efficiency gains but not full synchronization. When compliant digital money is integrated into DLT-based infrastructure, delivery-versus-payment becomes a system property rather than a coordination exercise.

The competition between stablecoins, e-money tokens, tokenized deposits and central bank digital currencies is not ideological. It is infrastructural. The model that combines accessibility, programmability, regulatory certainty and institutional trust will determine whether tokenized capital markets remain incremental innovations or evolve into fully integrated digital settlement ecosystems.

– end –

References

- BIS (2024), Ahmed & Aldasoro, Public Information and Stablecoin Runs.

- OeNB / BCG (2025), Euro Money Tokens – A strategic opportunity for Europe’s digital monetary system.

- Deutsche Bundesbank (2020), publications on programmable money.

- Regulation (EU) 2023/1114 (MiCAR).

- Directive 2014/65/EU (MiFID II).

- Directive 2009/110/EC (E-Money Directive).

- OeNB / BCG (2025), market capitalisation data on regulated stablecoins.

Further articles for you:

Why the next leap in efficiency is not called tokenization but collateral mobility

Tokenization alone does not create efficiency. What truly matters is that tokenized money market products can move seamlessly as collateral within regulated, integrated markets.

The state of tokenization

Tokenization is no longer an abstract concept but an infrastructural evolution in which assets are implemented as digital, executable market objects on DLT.

The state of tokenization – Part 2

The focus shifts from definition to execution: DLT, smart contracts, and regulated infrastructures demonstrate how tokenization is already being adopted at an institutional level.